Over a year ago we looked at what a credit score is and what can ultimately affect it. Some of the key takeaways from our last blog were:

- Pay off your balances, and pay them off on time. Consistency is key here.

- Do your best to use less than 30% of your available credit if at all possible. Overusing your credit card can be a red flag, and will eventually lower your score.

- Consider keeping old credit cards that you no longer use even after you’ve paid them off.

However, with it now being 2022, the emergence of Buy Now Pay Later and people perhaps having to borrow more than they would usually due to the cost of living increasing so dramatically, I thought now would be a great time to revisit some key points that can impact your credit score and how keeping an eye on your credit score is more important than ever!

Payment History

A key point and still very important, is that lenders and other financial institutions want to know that you can be reliable. If they offer you a loan or other finance, they’ll want to make sure that they’ll get their money back. It’s as simple as that. Consistency in paying off your balances on time is crucial to building and maintaining a great credit score. Keep in mind that If you regularly miss payments, your credit score will drop with time. This is why with the news that Buy Now Pay Later (BNPL) arrangements that you have will start to appear on your Credit Report you need to ensure you keep up to date with all your payments. Ensuring you have direct debits set up to pay the minimum payment* on your credit card(s) is a great tip along with making sure the dates the direct debits leave your account always coincide with after you are paid will help ensure that payments are never missed (missed payments can stay on your report for years so it’s a great and easy one to manage).

*Remember that paying off just the minimum payment due each month on your credit card(s) will take much longer to pay off the balance.

Credit Utilisation

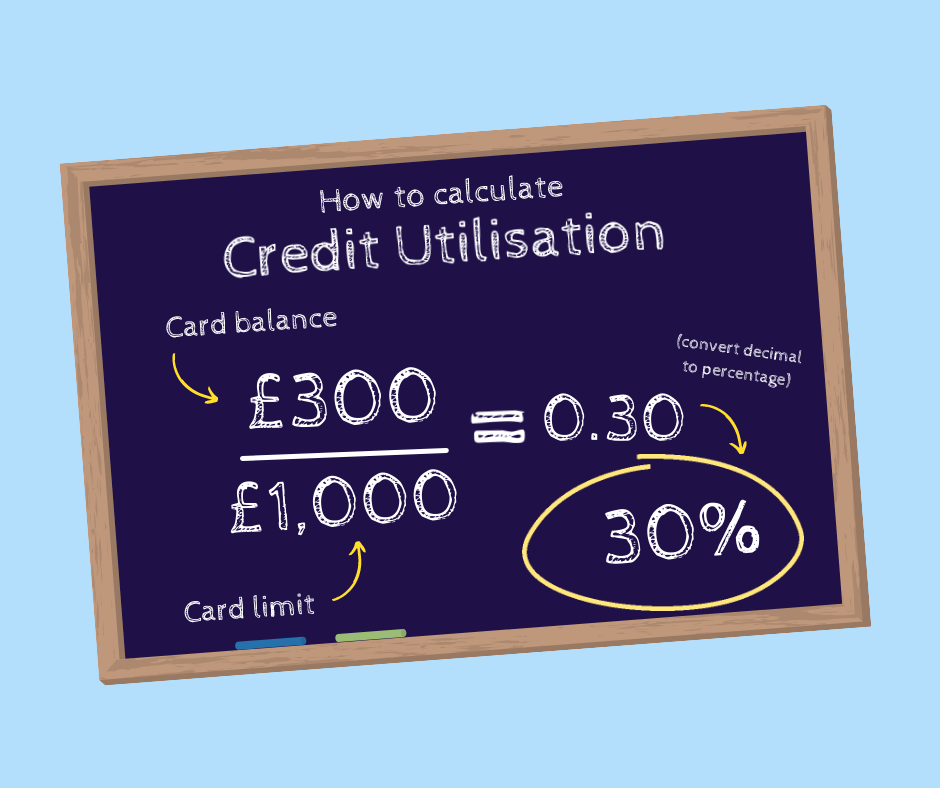

The second most impactful factor that contributes to your credit score is your credit utilisation. For those of you who may not be familiar with this term, we’ll break it down for you. Simply put, your credit utilisation is how much of your available credit you’re using at any given time. This can be expressed as a percentage, and is super easy to calculate! Check out an easy explanation below:

To work it out yourself, just take the balance you owe on your credit card(s), and then divide that by your credit limit(s), and you have your credit utilisation rate!

The reason it is suggested to keep your credit usage to a certain % is because the less credit you use, the less likely you are to appear totally reliant on it. Instead, it will look more like credit is a tool that you strategically utilise, and that’ll be a positive sign to lenders or creditors! Over time, this will also help to improve your credit score. Do note that on some Credit Reporting websites it does suggest using less than 50% of your credit utilisation so it can vary slightly from provider to provider.

Credit History

The third most influential factor that can affect your credit score is the length of your credit history. A longstanding credit history can speak volumes to a lender or financial institution when you’re in consideration for a loan, and this will be reflected in your credit score. Keep in mind, however, that a long credit history alone won’t do anything for your credit score if you have a track record of late or missed payments. For those who are just starting out and don’t have a long credit history, it is not something to panic about just yet as long as you make your payments on time your credit score/history will gradually build over time.

One other factor to consider here is what to do once you’ve paid off credit cards that you no longer plan on using. Leaving these cards open can actually help increase your credit score over time. Cards that you keep open but no longer use can still show up on your credit report for years, and their age alone over time can help boost your credit score. It is a top tip from most companies to never close a credit card even if you do not use it, as remember the Credit Utilisation % above, an open card with no credit used will help go towards your Credit Utilisation % and actually help you.

Do remember with BNPL starting to appear on some Credit Reports too, now is an even more important time to ensure that you are keeping an eye on your Credit History and not just your current Credit Report too.

Dark Web and your Details

One use of your Credit Report which may slip under the radar is checking your Credit Report to see if there have been any loans/Credit Applications made in your name recently, which you have not made. This is a great way to see if your personal details have been used fraudulently to try and obtain credit. A great additional tool that we offer our customers is our Dark Web scan, which scans the dark web to see if any of your details have been found and then provides you with a monthly estimate of your risk level and the types of data that has been found as well as help and tips to ensure you keep your data safe.

Remember, lots of applications for credit (especially if they are denied) over a short space of time will impact your Credit Score and your Credit History as all searches and applications are recorded.

So it’s very important to ensure only applications that you yourself have made are appearing and your details are not being used by someone else. Signing up to ScoreMatter will not only allow you to keep track of your Credit Score but also help ensure your details are not on the dark web to be misused by fraudsters.

We hope our little revist on factors that impact your credit report has helped and be sure to check out our new blog which will be out next month!